With Q3 2015 in the books, Voit Real Estate Services has published their in-depth market reports for the Orange County and Mid-Counties industrial markets.

We’re happy to make these reports available to you on this page, as well as our commentary on what Q3 has shown us about the future of these markets.

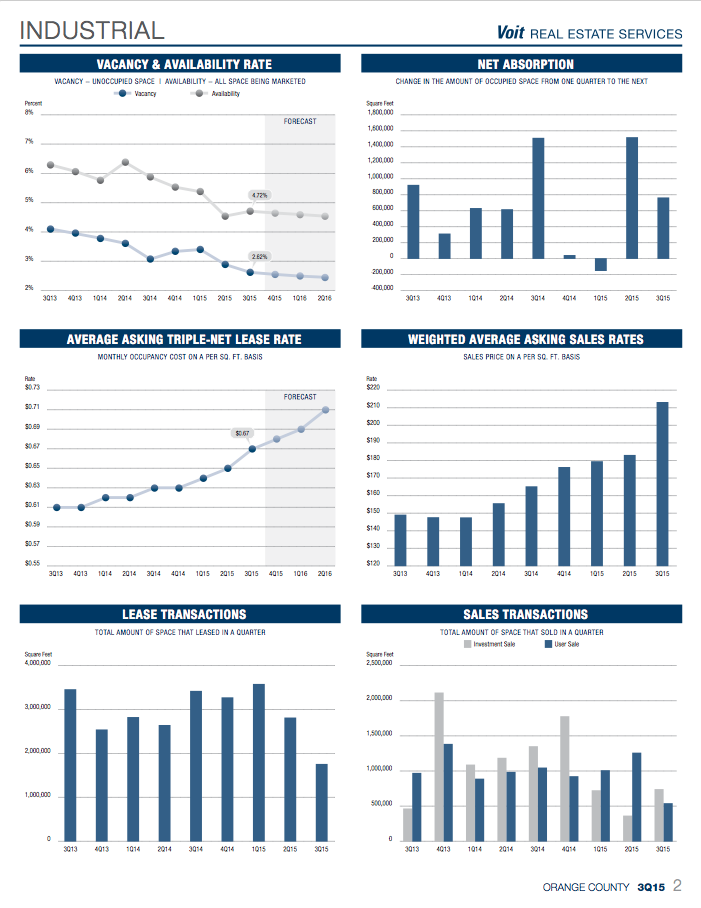

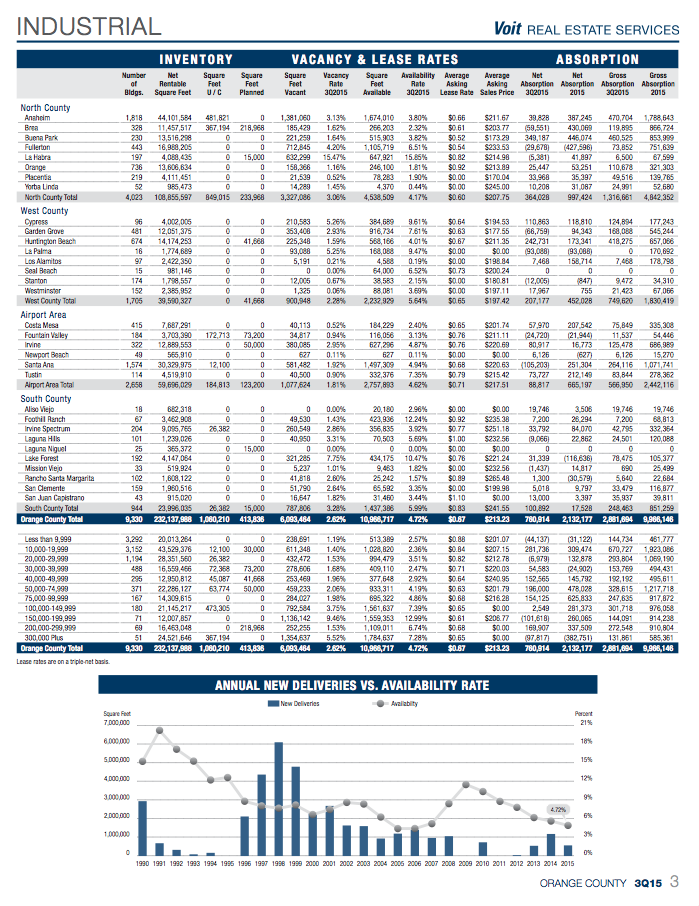

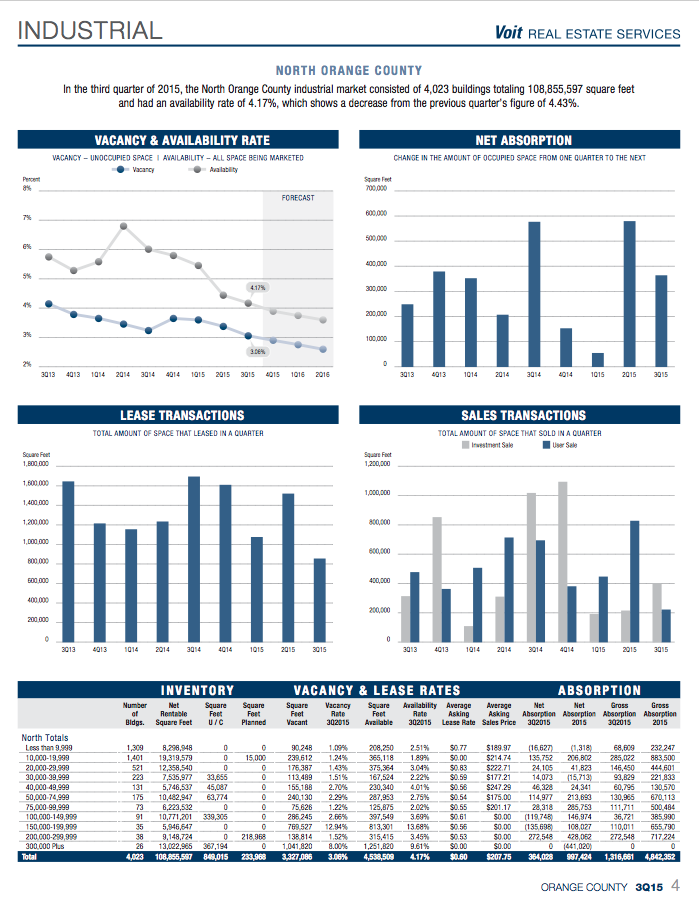

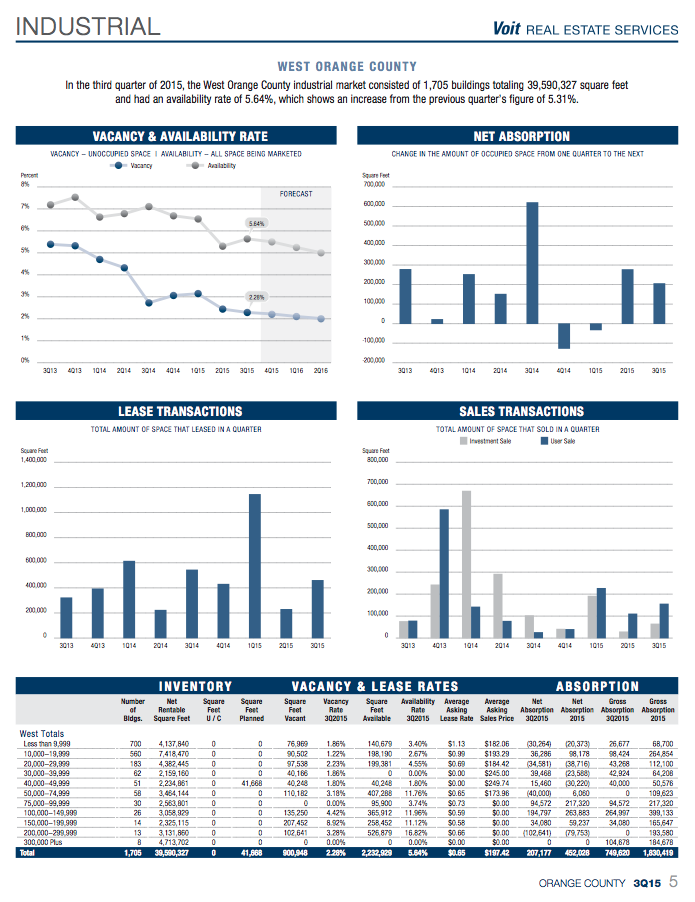

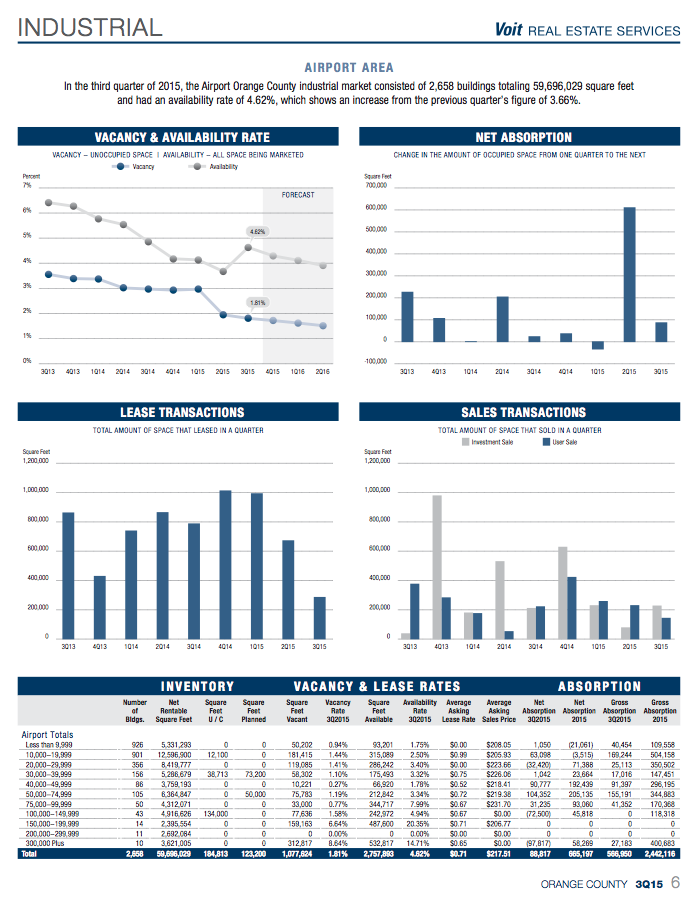

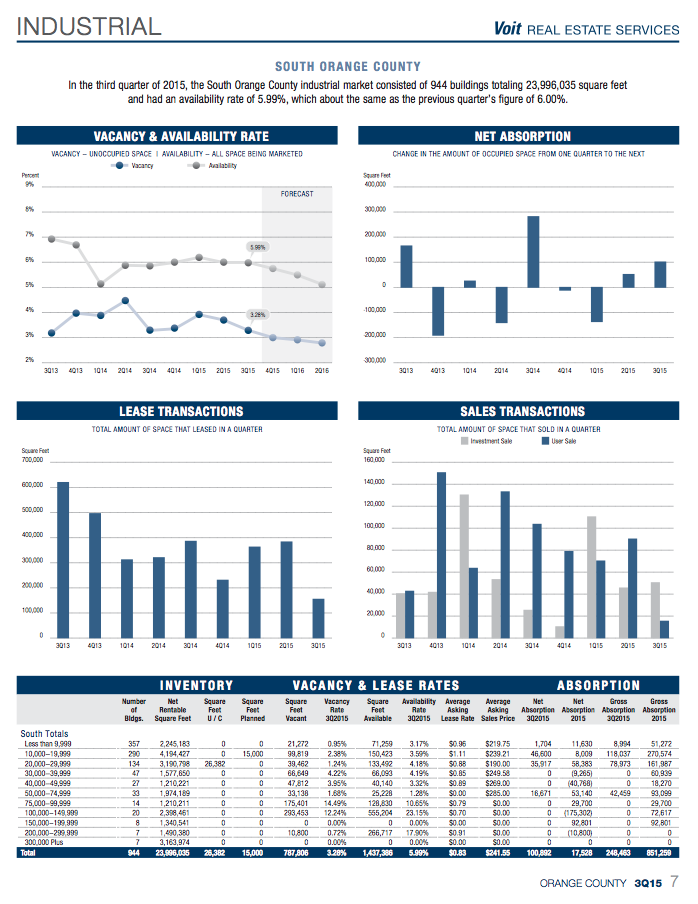

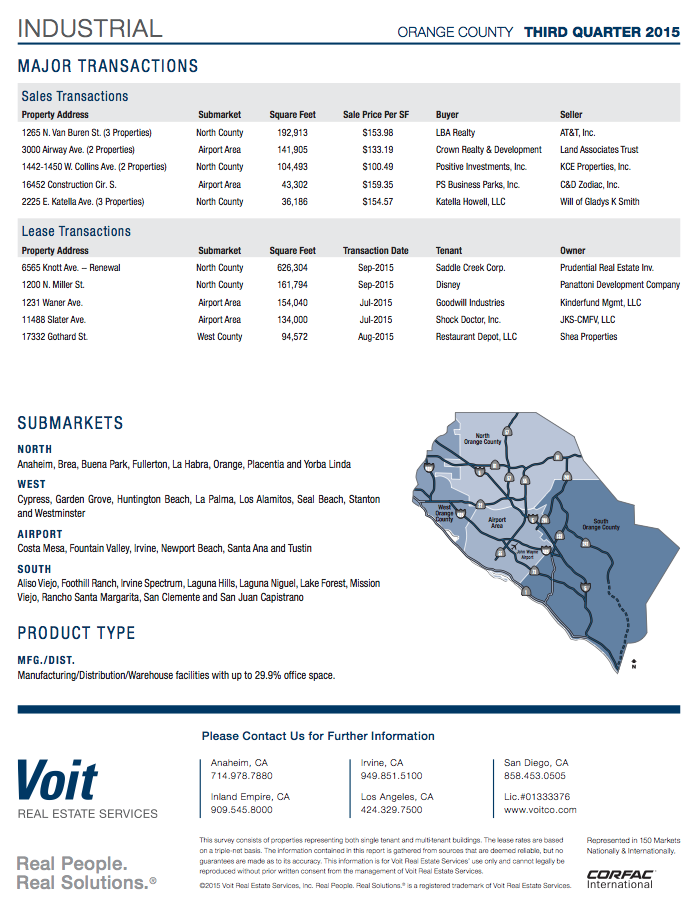

ORANGE COUNTY – INDUSTRIAL

OC Industrial Market Activity Hits the Brakes

The biggest news of the quarter is the impact that low supply is having on gross and net absorption, both of which have declined year-over-year. Fewer deals are getting done because there’s just no place to go for so many growing companies, and they are being forced to either shelve expansion plans or find new efficiencies within existing locations to boost revenues. Gross sale and lease activity, is off by nearly 47% compared to Q3 of 2014.

For over three years, this imbalance between supply and demand has been driving all the key market metrics. Even at the bottom of the last real estate cycle, vacancy hit a high of only 6.33%. Since then, it has fallen like a stone to its current level of just 2.62%, down another 27 basis points in just 3 months.

The average asking lease rate moved up another $.02 to $.67 in Q3, which brings the year increase in asking rents to 6.35%, four times the rise in the Consumer Price Index. Sales prices moved up again, as well. The number of options at any price point has been reduced to near zero depending on submarket and size range. So, tenants and buyers are advised to remain apprised of conditions in their local markets and allow up to a year to complete the relocation process.

Unfortunately, construction of new inventory is essentially non-existent, which leaves only the existing inventory to choose from. With 98% of that space currently occupied, tenants and buyers can expect to pay more for lesser quality, and spend more time looking for it.

Full Report

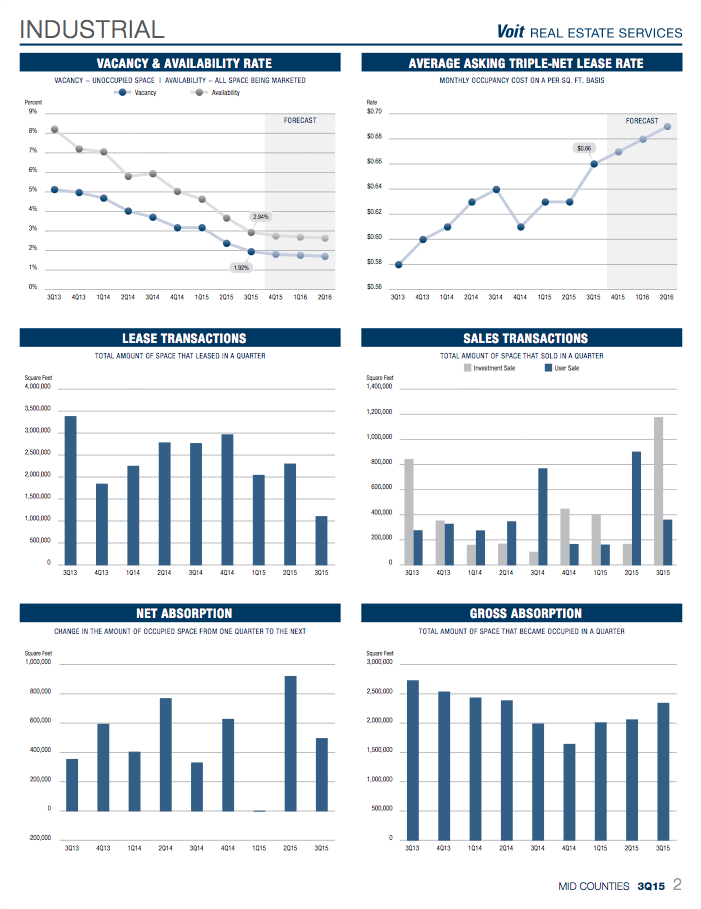

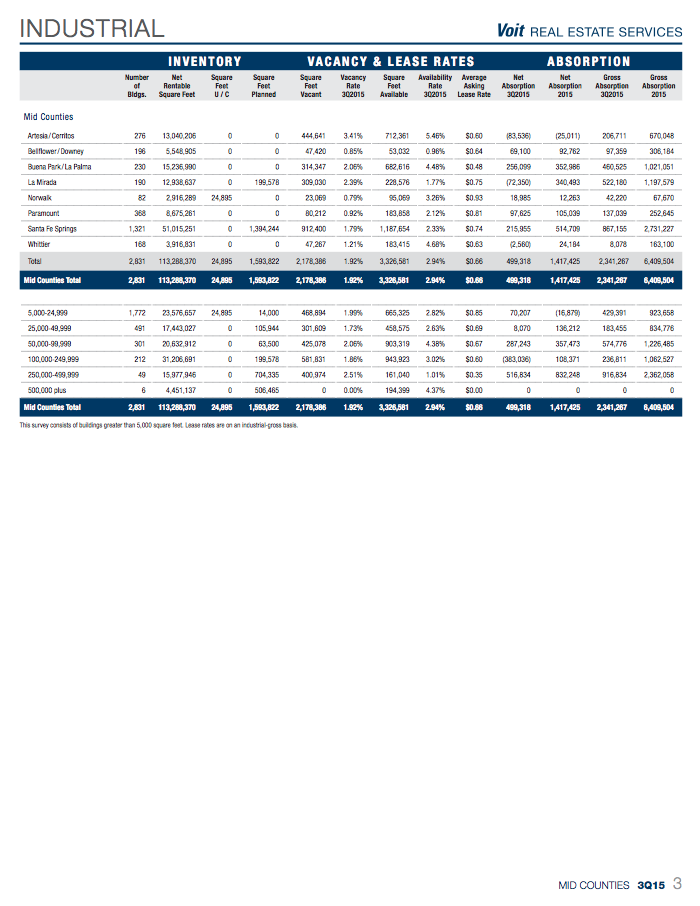

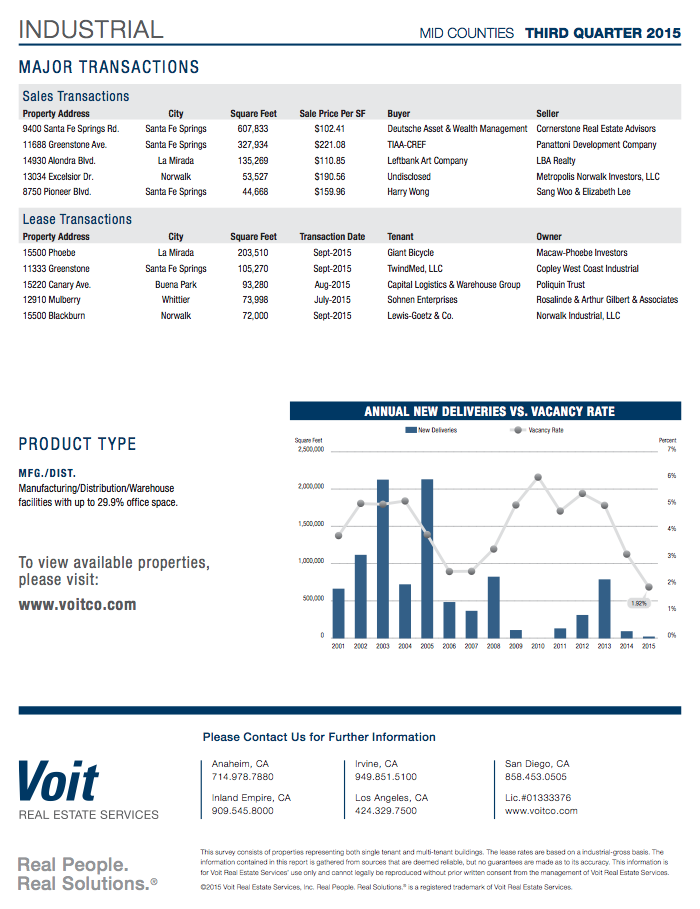

MID-COUNTIES – INDUSTRIAL

Vacancy Goes Sub-2 in Q3

For the first time ever, the vacancy rate in the Mid-Counties industrial market has fallen below 2%, which poses a further challenge to businesses who need to remain in the area to maintain competitiveness and boost revenues.

Competition from multiple bidders for properties offered for lease or for sale, is intense, and that has kept lease rates moving up. In Q3, the average asking lease rate rose another $.03 to $.66 on a NNN basis. But, price is not the biggest problem right now. Tenants and buyers are quite willing to pay the premium if they can just find a building that fits their needs.

With just 24,000 square feet of construction in this 113,000,000 square foot market, it is clear that holding out for a new building to satisfy a requirement will be a very long wait. That, compounded with the aging base of existing facilities, makes things even tougher. Functional obsolescence has become the rule not the exception, as much of the space that does hit the market was built more than thirty years ago, and landlords are in a position to say no to major improvements to accommodate new tenants.

The resulting decline in net absorption and transaction velocity has been expected, and there are no signs of relief in sight. Some companies are being forced out of the area while others are renewing in current locations despite the inefficiencies or adding secondary locations to meet short-term needs.

Full Report