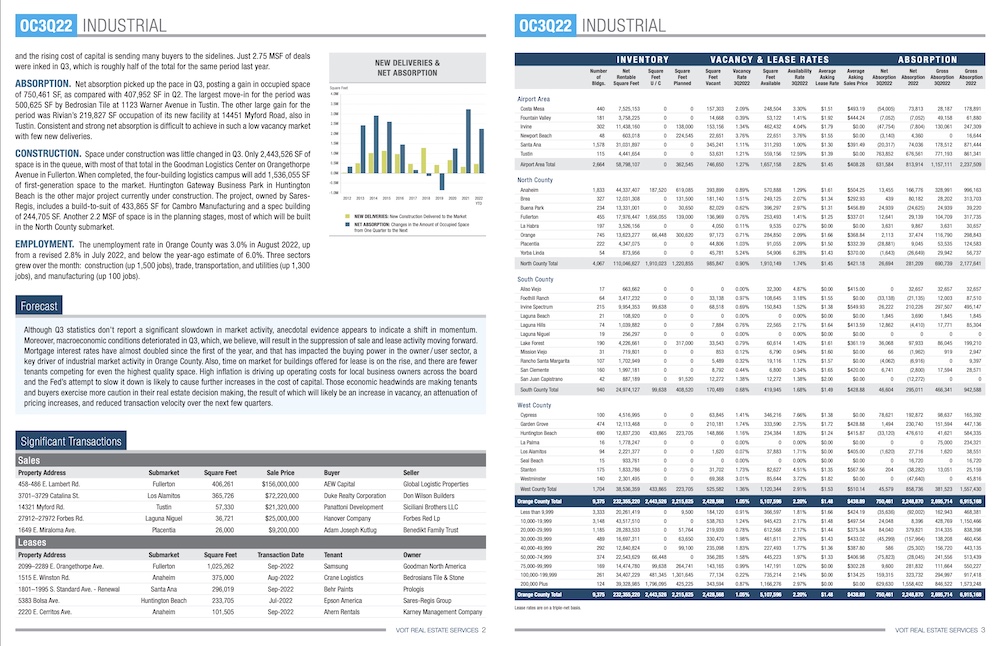

Q3 results for the Orange County and Mid Counties regions still reflect tight market conditions caused by persistent low vacancy and the absence of sufficient new deliveries to meet demand.

However, market metrics are a lagging indicator and don’t reflect current market activity, which weakened during the period. Mortgage interest rates have skyrocketed for both conventional and SBA financing, and that threw a wet blanket on sales activity for new investment and owner/user deals. Institutional level sales activity has hard hit with most deals being re-traded in escrow due to the almost daily increase in the cost of capital. Owner/users looking to finance through the SBA 504 programs are looking at rates above 6.5%, nearly double the rate offered less than a year ago.

Leasing activity is also trailing off, though lease rates have yet to see a decline. Competition for space has diminished. Gone are the days of 5 or more offers at a time, a years-long phenomenon that has driven lease rates to record highs. Buildings are taking longer to lease as a result of reduced tenant activity and listing brokers are seeing fewer inquiries and property tours, a clear indication that the balance of supply and demand is undergoing a fundamental shift. Time-on-market is now measured in months rather than week or days. This is welcome news to tenants who have to make moves in the next few months, and it also gives those not in a hurry a chance to take their time in anticipation of softer market conditions moving forward

General economic conditions also deteriorated during Q3. High inflation is firmly embedded and the Fed has made clear its intention to keep moving its benchmark Fed Funds Rate higher to get it under control. This will force mortgage rates for commercial property loans even higher in the coming months, which will likely result in price declines for owner/user buildings and the decompression of cap rates on investment properties.