As we look ahead to 2016 in the Southern California industrial markets, one indispensable tool has been Voit Real Estate Services’ newly published Q4 2015 market reports.

These in-depth reports round up the performance of the Orange County and Mid-Counties industrial markets in the final months of 2015, and include all the fully-illustrated and graphed data you would expect from Voit.

We’re happy to make them available to you on this page for browsing and downloading, along with our commentary on what Q4 has shown us about the future of these markets.

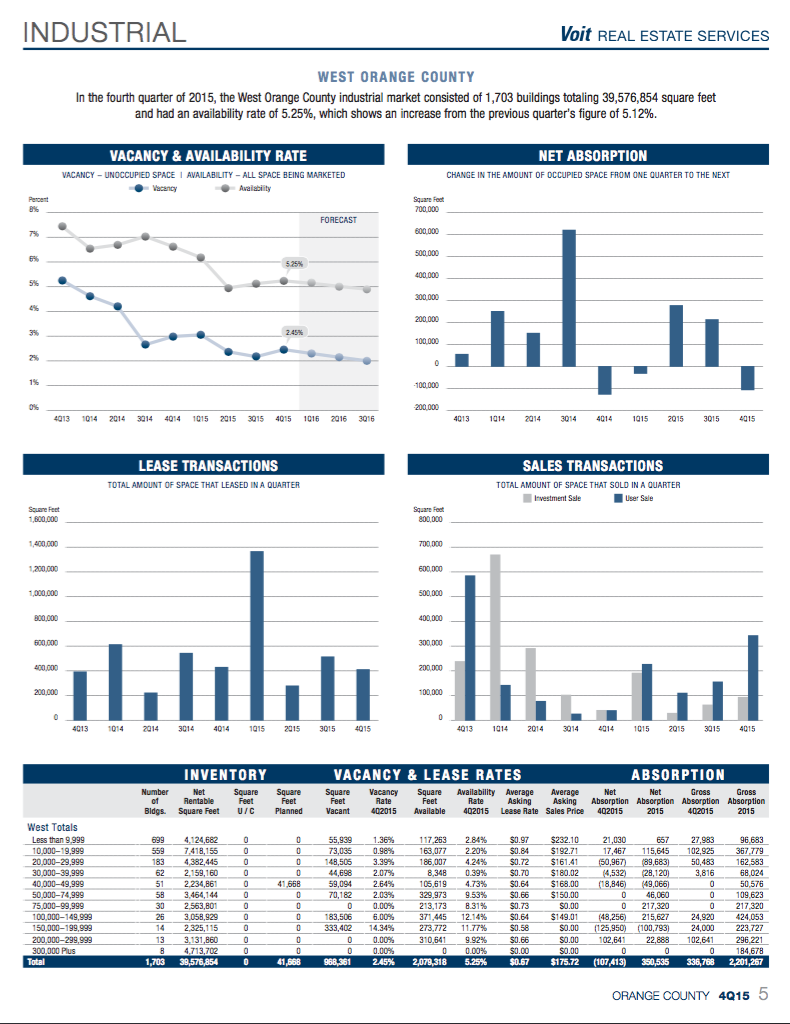

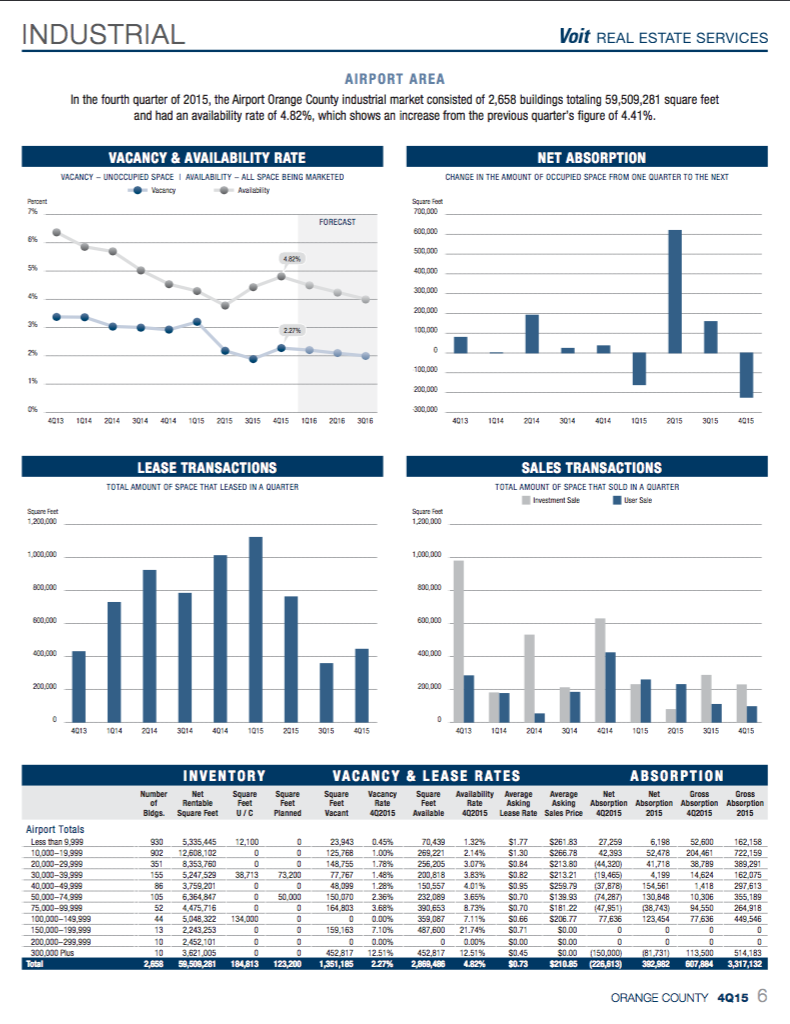

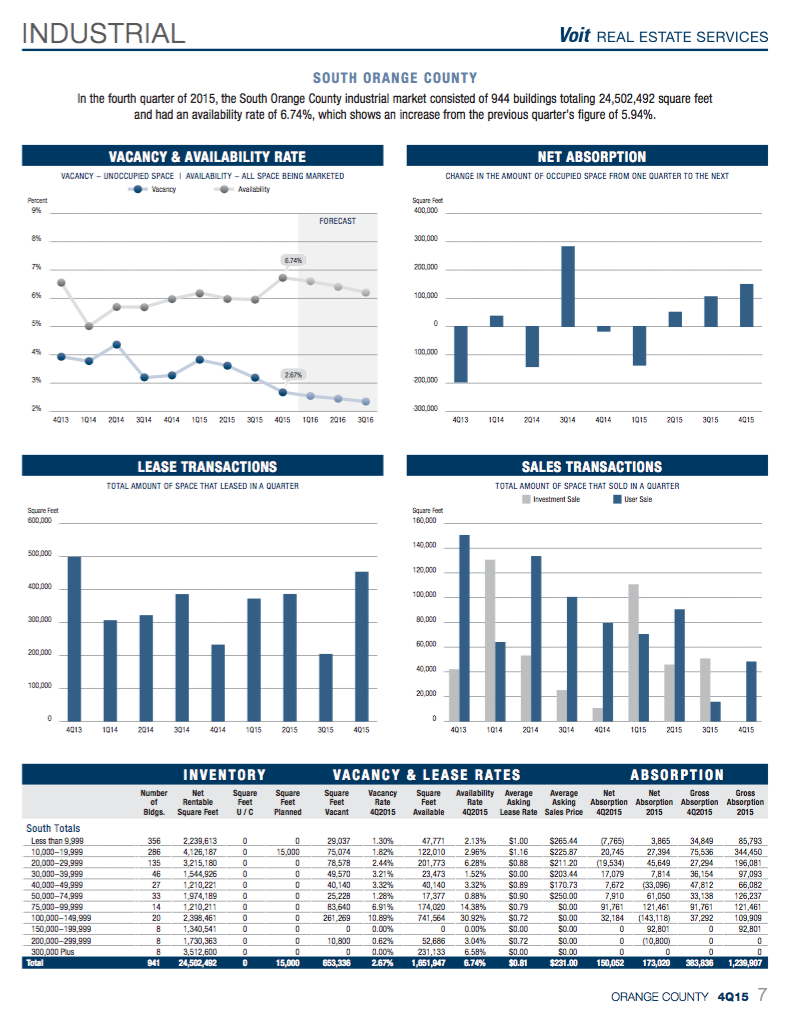

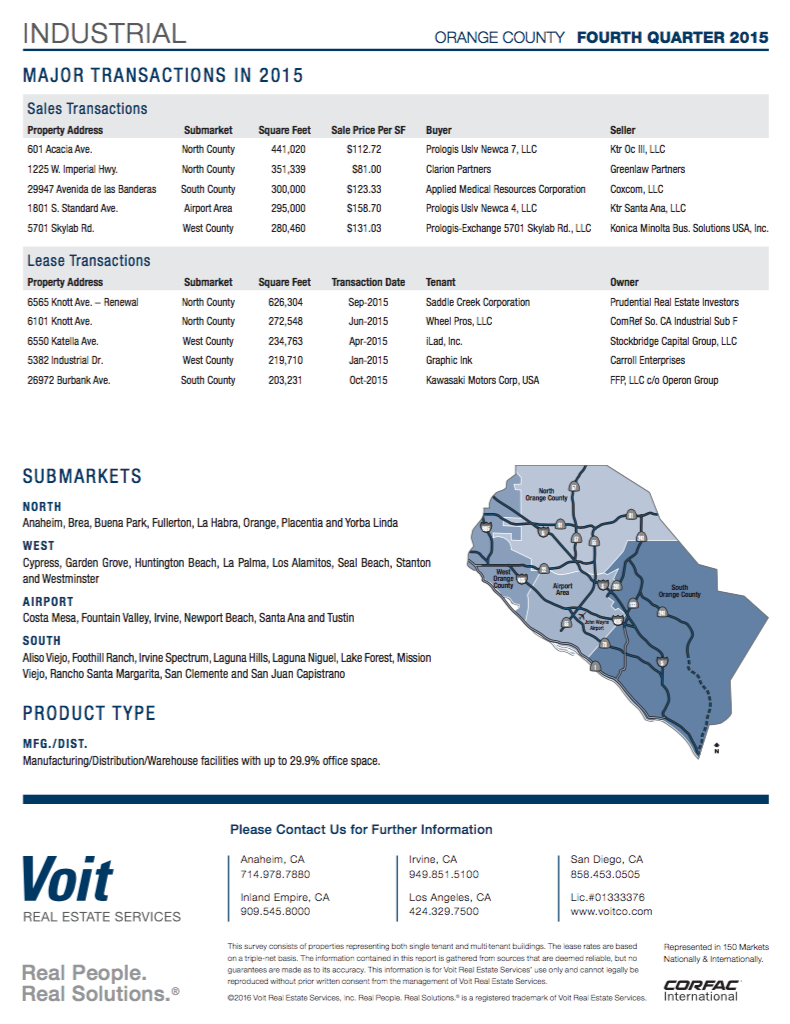

ORANGE COUNTY – INDUSTRIAL

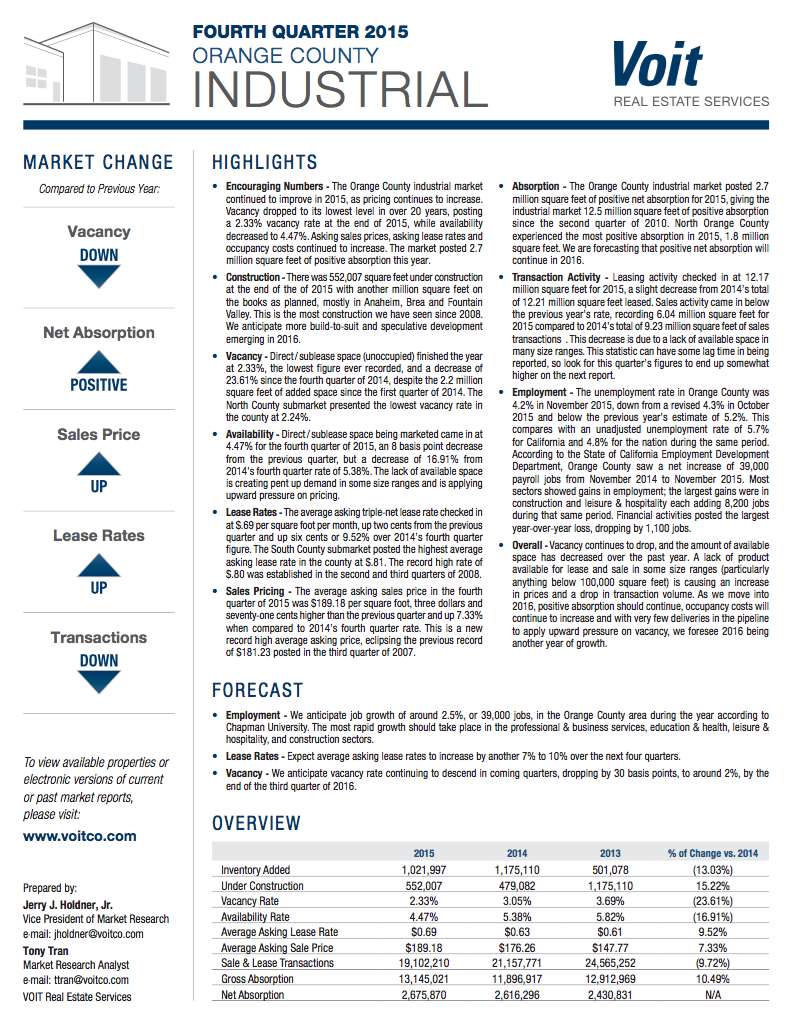

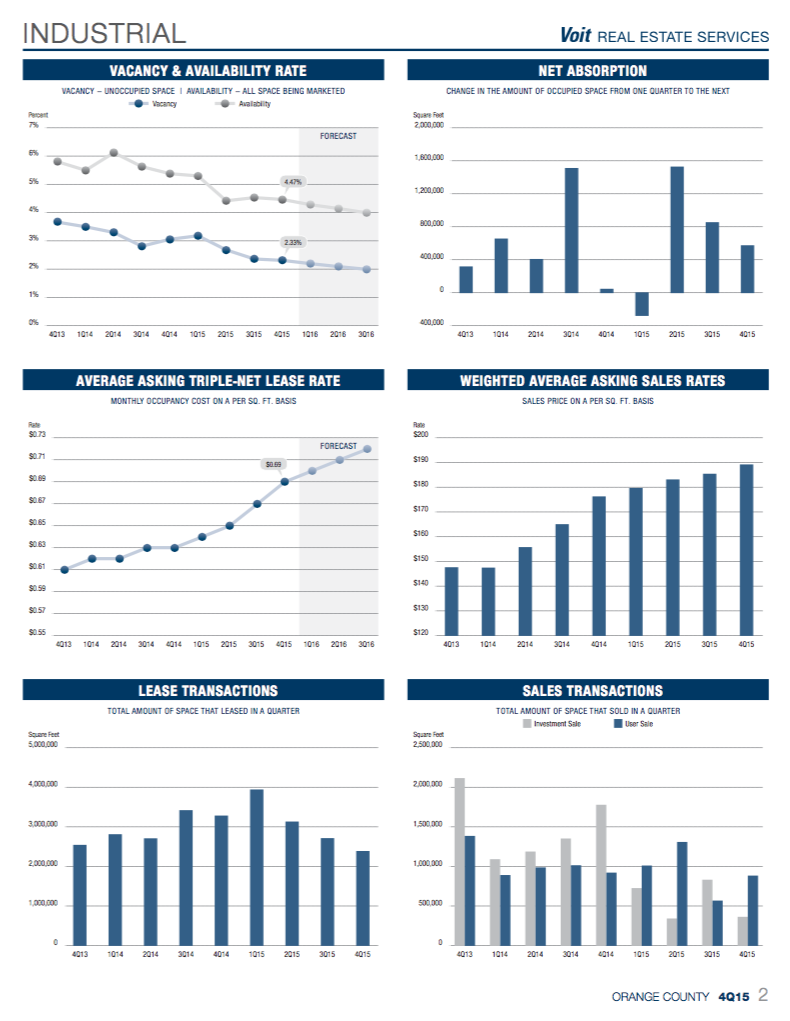

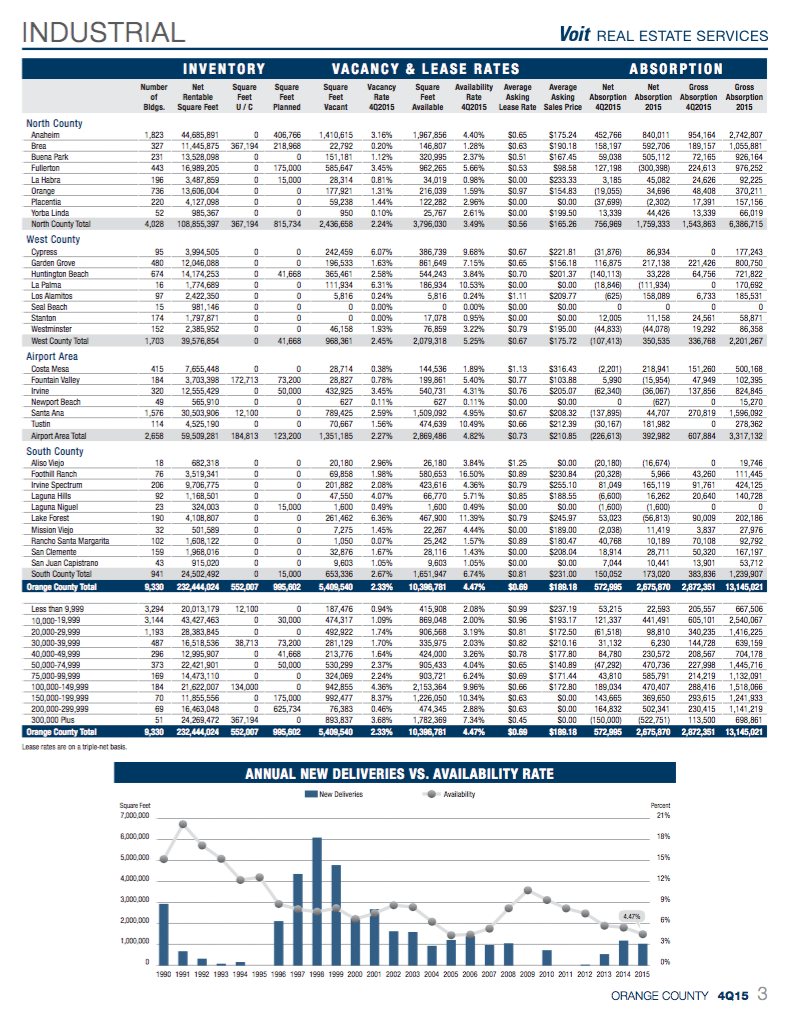

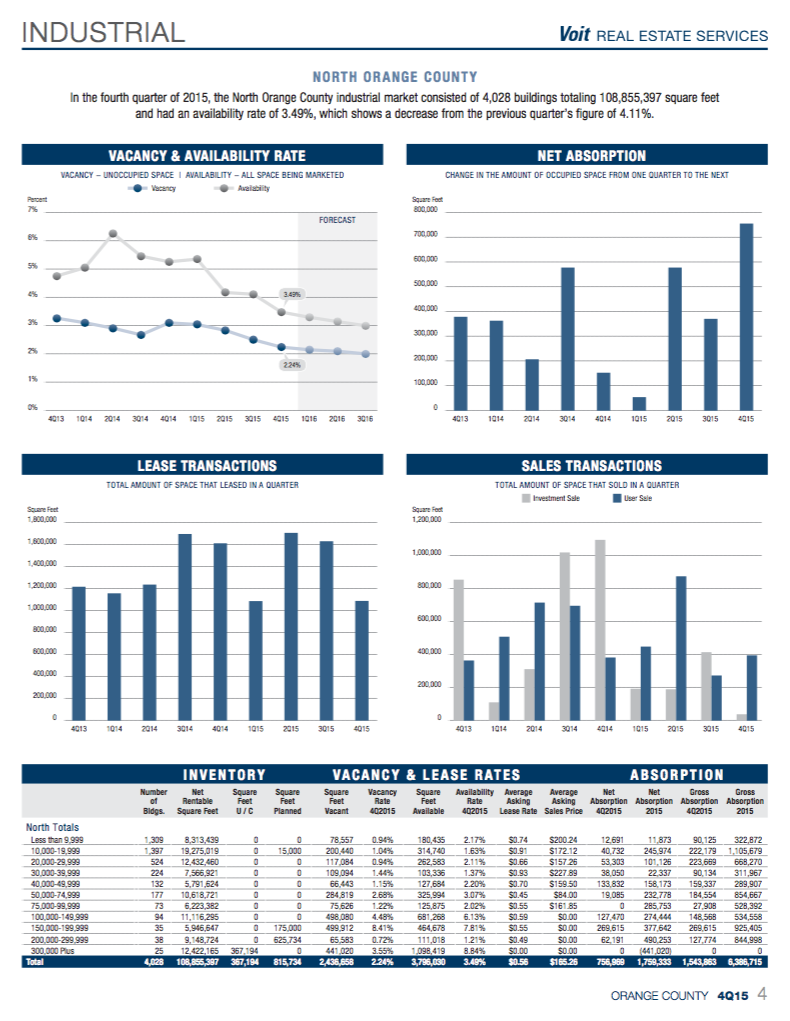

Orange County’s Big Squeeze Continues in Q4

Q4 brought no relief for beleaguered business owners who just can’t find quality space that fits their needs.

This has been an ongoing problem, and nothing in the latest statistics point to any different as we move into 2016. Landlords are still calling the shots in the leasing market, as they are feeling confident about pushing for higher prices and longer lease term while offering less in the way of concessions.

Title 24 regulations have driven improvement costs up and that is compounded by the fact that more renovations are necessary for the older product that tenants have to choose from.

The average asking rate for Orange County moved up another 9.5% in 2015. So, tenants essentially paid more to get less. It’s gotten to the point where business owners should be on the lookout for their next building all the time, no matter when their leases may be expiring.

The sale market has been no kinder to buyers. The average per square foot sales prices eclipsed the high of 2007 and prices are still moving up due to short supply. Development is still at a near standstill because land is scarce and prohibitively expensive. The limited supply of new product that does find its way out of the ground will be in the upper size ranges.

Full Report

MID-COUNTIES – INDUSTRIAL

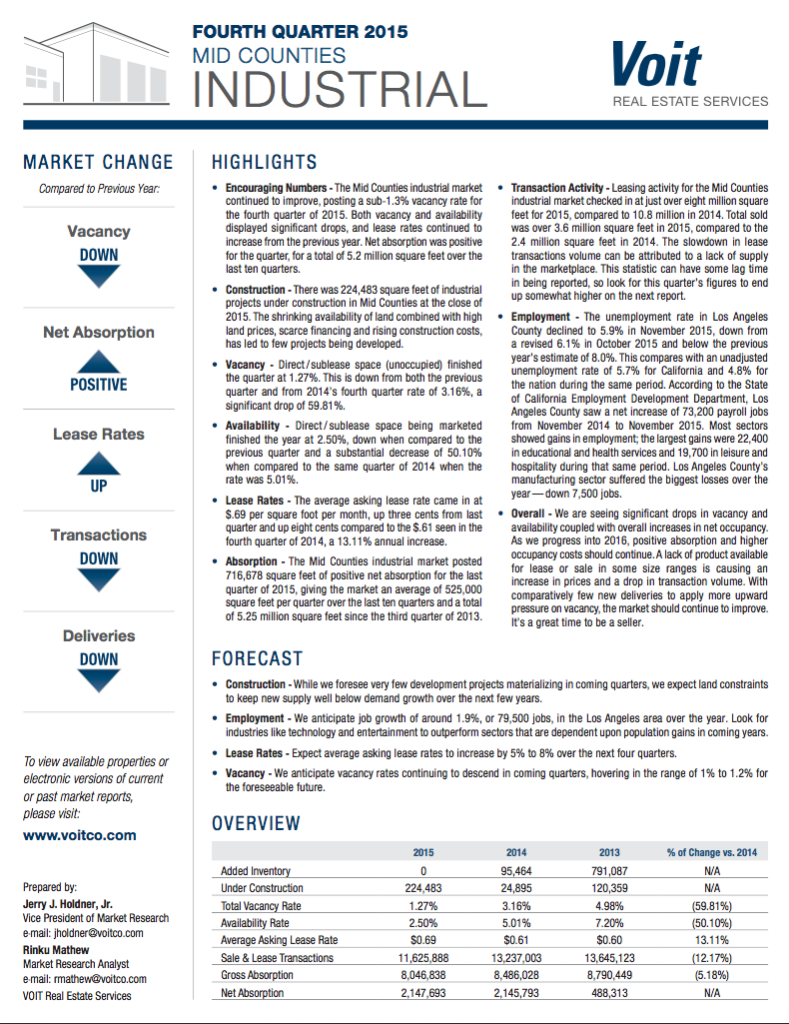

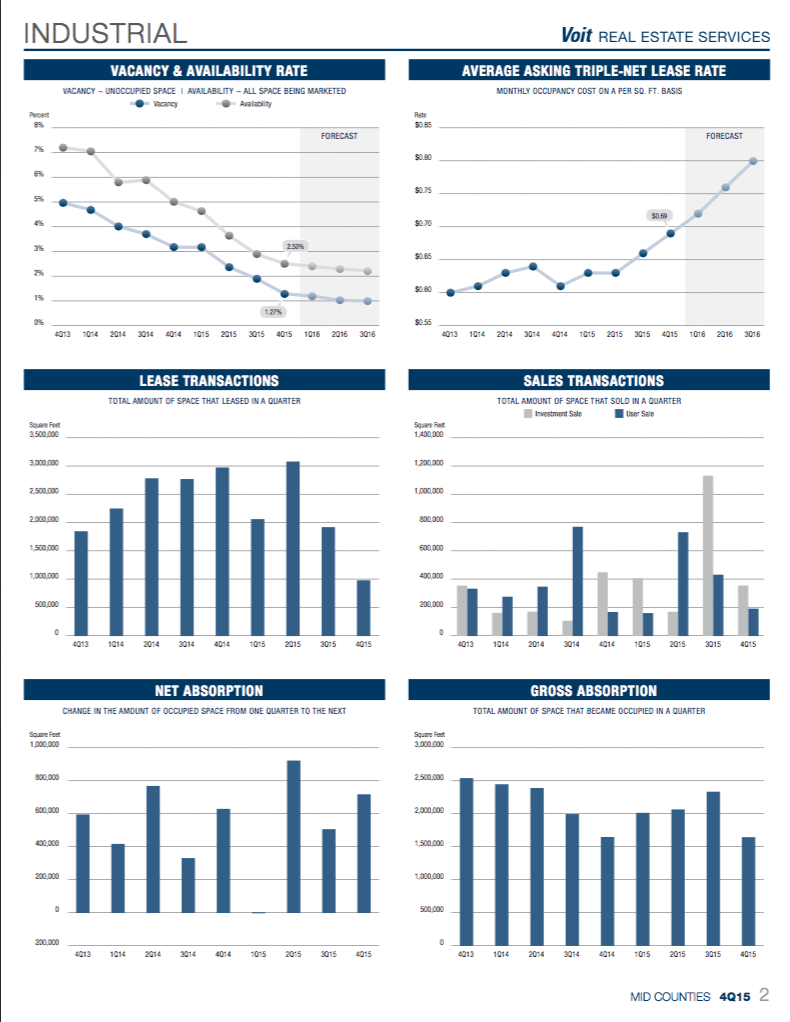

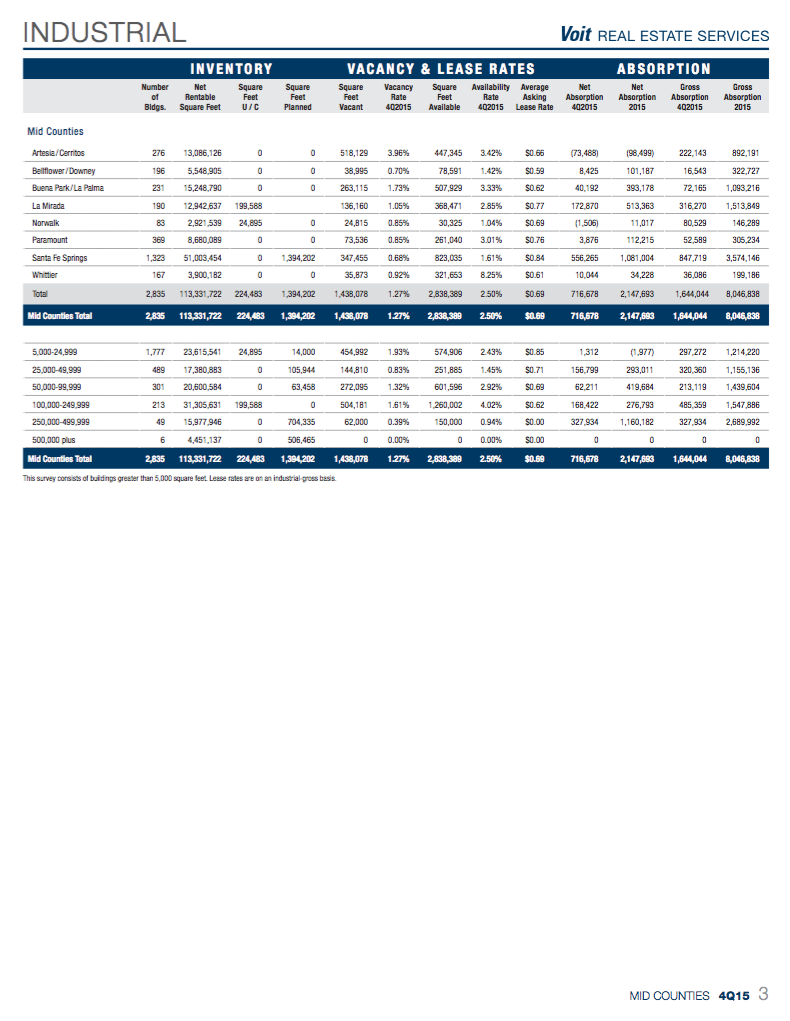

Mid-Counties Vacancy Hits New Low

Just when we thought the vacancy rate in the Mid-Counties industrial market couldn’t go any lower, it did.

By the end of Q4, just 1.27% of the industrial inventory was unoccupied, compared to 3.16% a year ago. That made a big problem even bigger for expanding business in this strategically located market that serves both parts and most of Southern California. Users who are there want and need to be there, which complicates the problem.

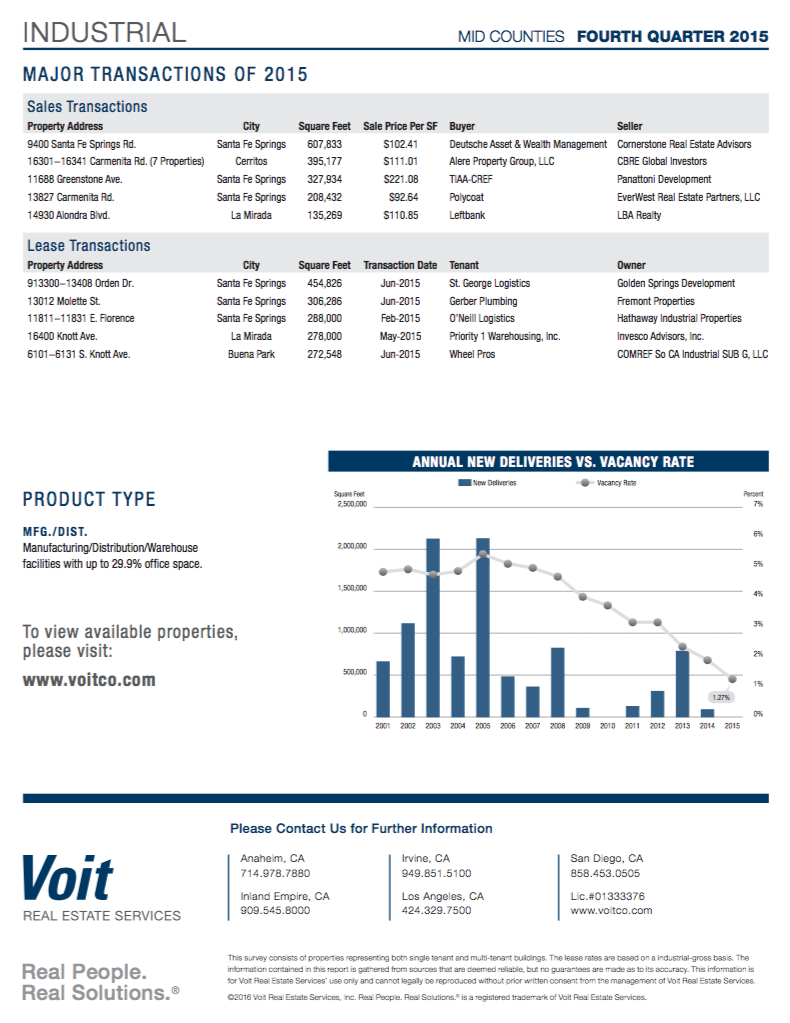

These businesses can’t just pick up and leave without putting their revenue at risk. So, they just keep paying more for aging inventory even if it does not allow their operations to function at peak efficiency. New construction activity is nominal and concentrated in very large distribution facilities, which is no help to the vast majority of users who occupy spaces under 100,000 square feet.

The result; transaction volume fell sharply in 2015 because there was simply no place to go.

The sale market is just as tight. Prices moved up another 7.73% during the year, after multiple years of double-digit increases. Demand is still at an all-time high and no new product is being constructed that will be offered for sale. Any owner willing to sell his property in 2016 can expect to get a lot of attention and command a very high price.

Full Report

Leave a Reply

You must be logged in to post a comment.